Since 2017, the guys from Data Leakage & Breach Intelligence have been reviewing the domestic breach market by year. Now another one has arrived, which has several very remarkable moments.

1️⃣ The cost of “breaking through mobile operators” increased over the year by an average of 3.3 times.

2️⃣ “Gosprobiv” (all according to the State Traffic Safety Inspectorate, “Magistral”, “Potok”, etc.) is almost 8 times cheaper than “bank probiv”, although the price of “gosprobiv” has increased 2.5 times over the last 2 years.

3️⃣ Until now, the most popular are “state breakdown” and “mobile”. The overall market share of “bank breakout” is much lower.

Just in case, let me remind you that all this is absolutely illegal. And for understanding, I highly recommend paying attention to the graphs in the article. There you can clearly see the rise in prices in recent years and this is connected not only with inflation, but also with new risks faced by unscrupulous local employees (which is good). Just look at the practice of punishment for illegal transfer of information in the last couple of years.

for “mobile penetration” – by 17%.

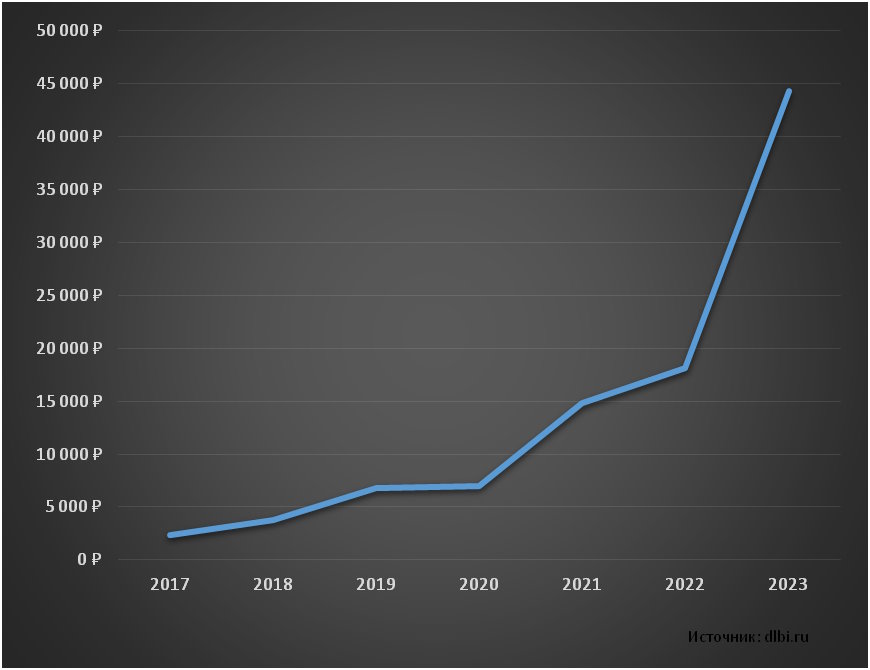

Since we have been keeping “breakdown” statistics since 2017, we can trace the dynamics of price changes over these years.

This graph shows the change in the median price of all the main types of “breakout” available on the market. A constant trend of rising prices from year to year is clearly visible. Over 7 years – 18.5 times. Moreover, the first significant jump in prices by 2 times occurred in 2021, and in 2023 prices increased by another 2.5 times compared to the previous year.

This probably suggests that until 2021, prices were mainly influenced only by inflation. Starting in 2021, prices are likely to be influenced by some of the measures organizations are taking to combat insiders engaging in illegal information trading. It is not possible to completely eradicate “breakthrough” as a phenomenon, but the complexity of obtaining information is increasing and, accordingly, prices from intermediaries are also rising.

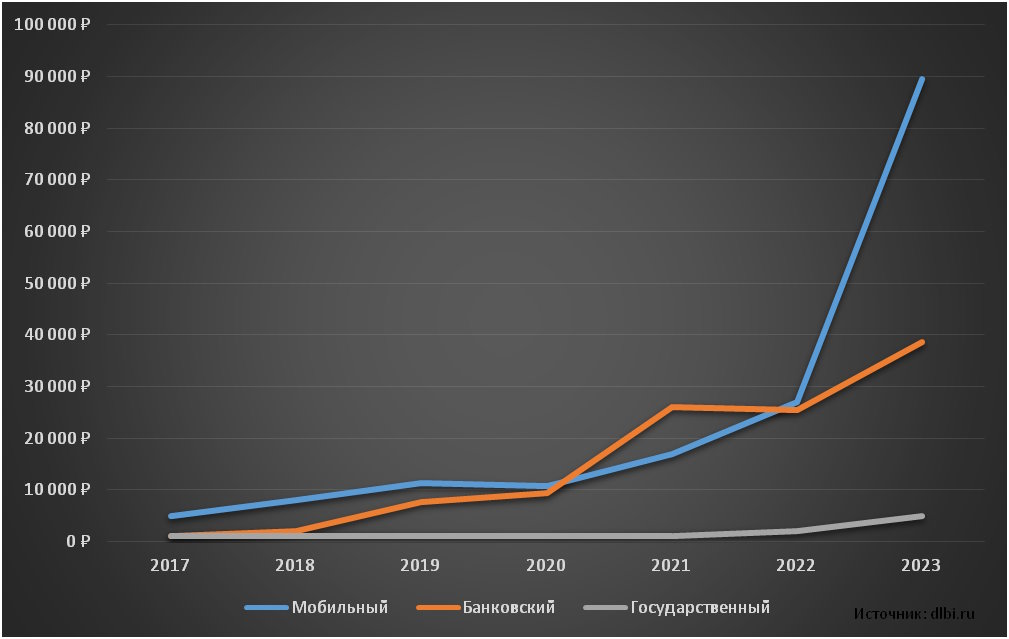

The chart below shows the median breakout price for three main areas: banks, mobile operators and government agencies.

As a reference “service” for “banking breakdown”, we traditionally selected a statement for a minimum period (a month or more, depending on what is available on the market) for the accounts/cards of clients of all banks for which there were offers for the reporting period. For “mobile penetration” – details of calls and SMS of subscribers for a minimum period (a month or more, depending on what is available on the market) of 4 telecom operators. For “gosprobib” – obtaining information about the owner of the vehicle from the traffic police, the movement of a person from the “Rozysk-Magistral” system and data on all issued passports from the “Russian Passport” AS.

The price of a “breakthrough” according to state databases remains at a low level relative to other types of “breakthrough”. On average, “state breakdown” is almost 8 times cheaper than “bank breakdown”. Compared to 2022, prices for “state-produced goods” have increased 2.5 times. There are always plenty of offers of this “service” on the market.

The price of “breakthrough” for subscribers of telecom operators increased by 3.3 times compared to last year. “Mobile breakout” is 2.3 times more expensive than “bank breakout”. For the entire period of observation, only in 2021 was “mobile breakout” cheaper than “bank breakout”.

It should be noted that “services” ( flash , detailing , etc.) for “breaking through” subscribers are increasingly provided by intermediaries through their insiders in government agencies (the so-called “ request through authorities ”), and for most operators – only ” through the organs “. This is the most important change compared to last year and is probably why prices for “mobile breakout” have increased so much. There are also always many offers of “mobile penetration” on the market.

As for the prices for “breaking through” bank clients, after stagnation in 2022, in 2023 they increased by 51%. In comparison with “state breakout” and “mobile breakout”, “bank breakout” is still the most unstable “service” of this market. There may not be offers for a particular bank at the right time. For most small banks there is no “breakthrough” or it is extremely difficult to find. In fact, there is only one bank (see graph below), for which there is always a certain number of intermediaries (at the time of the study – more than 10) offering this “service”.

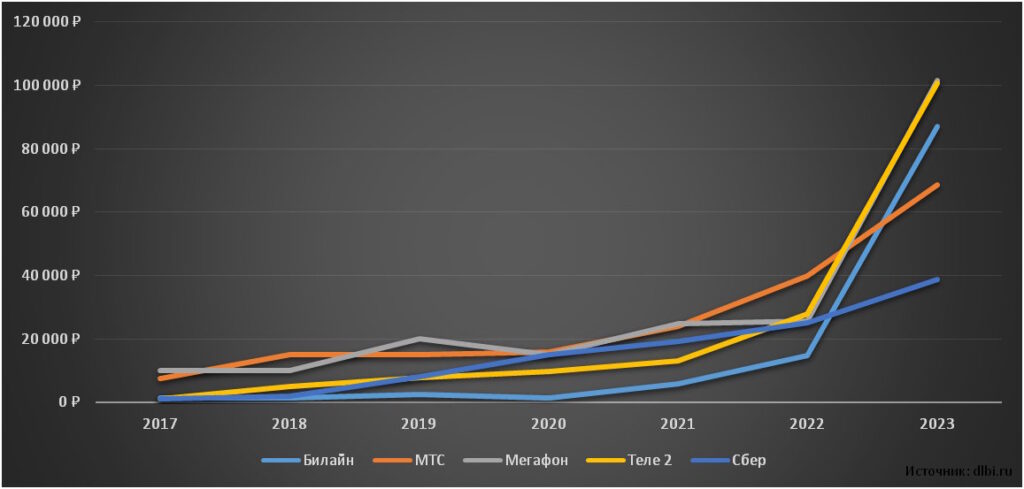

The following chart shows the median breakout price for specific companies.

Bank “breakthrough” is represented here only by SatThis is due to the fact that this is the only bank for which there is a stable “breakthrough” offer at any given time. For other banks there is no data (due to lack of supply on the market) for a particular year, and it is impossible to trace a continuous trend.

You must be logged in to post a comment.